Learning how long does it take to improve your credit score is an important step for anyone navigating the U.S. financial system. Whether you are preparing to apply for a mortgage, finance a vehicle, or qualify for better loan terms, knowing how these financial tracking timelines work can help you, plan your next moves more effectively. While some positive changes can impact your credit record data within 30 days, other strategic adjustments require several months of consistent financial behavior to reflect on your profile. The speed at which your credit history recovers depends heavily on data transmission cycles and the specific nature of the information listed on your report.

Table of Contents

The Core Timelines for Financial Recovery and Growth

Enhancing your rating depends heavily on lender reporting cycles and the information listed on your file. While some improvements appear quickly, long-term habits become increasingly important over time. Below are the detailed milestones and high-impact factors that determine the speed of your recovery:

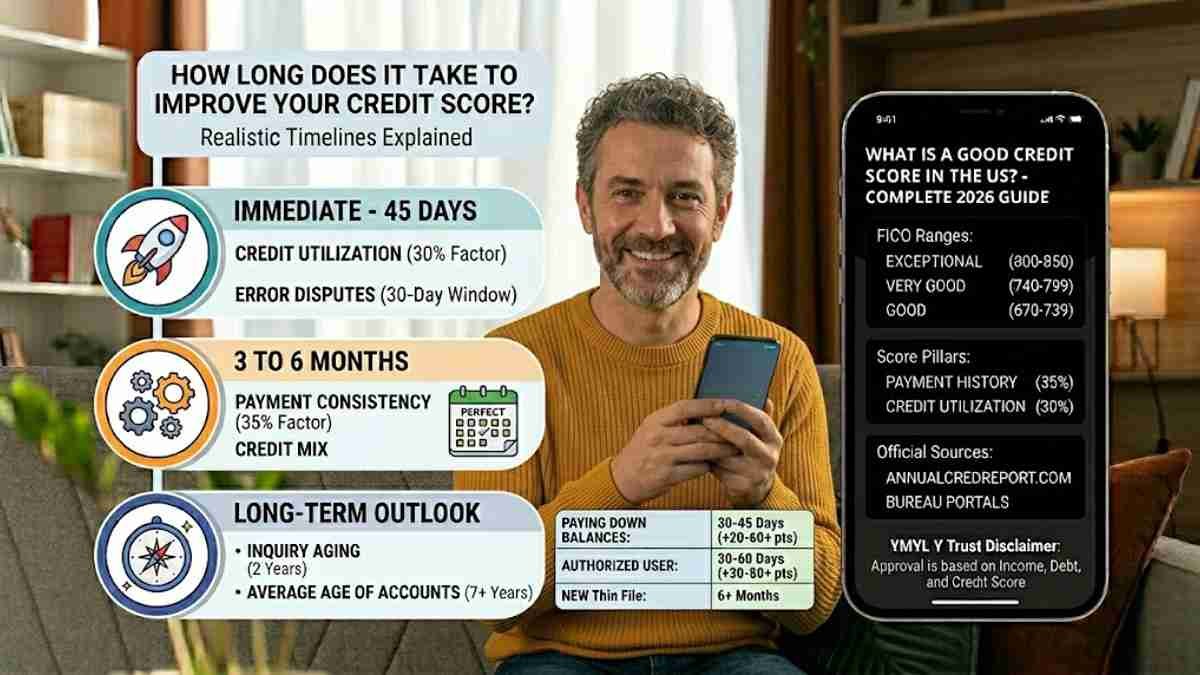

The Immediate to 45-Day Window: Reporting-Related Updates

- Reporting Cycles: Most lenders in the United States transmit data to Equifax, Experian, and TransUnion once per month, usually on your statement closing date.

- Utilization Shifts: If you pay down a high balance, the updated debt-to-limit ratio is typically reflected on your file within 30 to 45 days.

- Rapid Gains: Strategic balance reduction is often one of the fastest ways to see a boost because your standing is calculated based on your most recently reported balances.

- Error Correction: Under the Fair Credit Reporting Act (FCRA), credit bureaus generally have a 30-day window to investigate and resolve formal disputes.

- Dispute Outcomes: Successfully removing an inaccurate late payment or an unauthorized account can provide a substantial lift once the investigation concludes.

- Mid-Cycle Reporting: In some cases, you can request a “rapid rescore” through a lender. This can update your information in as little as 3 to 7 business days, though it is usually reserved for active mortgage applications.

The 3-to-6 Month Phase: Establishing Reliability

- Payment Consistency: Lenders prioritize a clean history; establishing a multi-month streak of on-time payments signals reduced risk to future creditors.

- Historical Data Patterns: Modern scoring models look at your financial behavior over a 24-month period, rewarding a steady downward trend in debt rather than one-time payments.

- Thickening a Thin File: For those with limited history, it typically takes at least six months of activity for a FICO score to be generated.

- Credit Mix Benefits: Diversifying your accounts, such as adding a small installment loan to a profile dominated by credit cards, begins to show positive weight after 90 days of reported data.

- Authorized User Impact: Being added to a seasoned account can reflect on your report in 30–60 days, allowing you to benefit from that account’s age and low utilization.

- Stable Residency and Employment: While not directly calculated in the score, lenders often look for 6 months of stability in these areas during the manual review portion of a loan application.

The Long-Term Outlook: Strategic Rebuilding

- Inquiry Aging: While hard pulls stay on your report for two years, their negative impact on your score usually diminishes significantly after 12 months.

- New Credit Stabilization: The “temporary dip” caused by opening a new account usually recovers within 6 to 12 months of responsible management.

- Public Record Recovery: While the record itself remains longer, the mathematical impact of severe marks like bankruptcy begins to fade after the first 24 months of positive post-filing activity.

- Long-Term Utilization Habits: Sustaining a credit utilization rate below 10% for an extended period is often required to enter the “Exceptional” (800+) scoring tier.

- Average Age of Accounts: To reach elite levels, your average account age usually needs to exceed 7 to 9 years, a milestone that simply cannot be rushed.

Strategic Analysis of Score-Moving Levers

To understand how long it takes to improve your credit score, it is important to understand how different scoring factors are weighted. Each factor has a different speed of impact based on how it is calculated.

The Utilization Lever (Fastest Speed)

Utilization represents 30% of your total score. Because it is a “snapshot” of your current debt, paying a balance today can result in a score jump as soon as the next month. This is the primary tool for anyone needing a quick boost for a looming loan application.

The Payment History Lever (Slowest Speed)

At 35% of your score, this is the most powerful but slowest factor to change. While you cannot “speed up” time, you can prevent further damage. Every month of on-time payments slowly dilutes the impact of a past late payment.

The Dispute Lever (Variable Speed)

If you find a major error, such as a foreclosure that isn’t yours, the recovery can be immediate upon resolution. Once the error is removed, your score may bounce back to its rightful level—often within 45 days.

Comparison: Timelines for Common Credit Actions

| Action Taken | Estimated Time for Impact | Potential Score Impact |

| Paying Down High Balances | 30–45 Days | High (20-60+ points) |

| Disputing Reporting Errors | 30–45 Days | Very High (50-100+ points) |

| Becoming an Authorized User | 30–60 Days | High (30-80+ points) |

| Using Alternative Data Boosts | Instant to 30 Days | Moderate (5-15 points) |

| Building from a Thin File | 6+ Months | High (varies by model) |

| Negotiating a Pay-for-Delete | 45–60 Days | Moderate to High |

The Lifespan of Derogatory Marks on Your Credit Report

While you can take proactive steps to improve your status, some items simply require the passage of time to be removed entirely from your file:

- Late Payments: These remain on your history for seven years from the date of the first delinquency.

- Collection Accounts: These typically stay for seven years, though newer models may ignore them once paid.

- Chapter 13 Bankruptcy: This remains on your report for seven years from the filing date.

- Chapter 7 Bankruptcy: This remains for ten years due to its severity.

- Hard Inquiries: These stay for two years, though they only influence your credit rating for one year.

- Foreclosures and Short Sales: These stay for seven years and significantly impact your ability to get a new mortgage for the first several years.

Strategic Monitoring: How to Track Your Recovery Timeline

To accurately track your progress and understand your specific situation, consistent oversight is mandatory:

- Monthly Routine: A standard monthly audit ensures that your recent payments and balance reductions have been officially recorded by the bureaus.

- Weekly Oversight: If you are in an active recovery phase or preparing for a mortgage, weekly checks allow you to see exactly when an update is reported.

- Official Data Access: Use AnnualCreditReport.com to obtain full reports and verify that your payment history is being represented accurately.

- Score Tracking: Utilize your bank’s integrated FICO score tracking to see how these updates translate into the numerical value lenders see.

- Identity Protection: Real-time alerts are crucial; a single fraudulent account opened during your recovery phase can set your timeline back by months.

Frequently Asked Questions

How long does it take for your credit score to go up after paying off a debt?

It typically takes roughly 30 to 45 days for a recent payment to reflect on your credit profile. This timeframe exists because most major lenders and credit card companies transmit account data to Equifax, Experian, and TransUnion just once a month, usually near your statement closing date. Once the lender updates your information with the bureaus, the drop in your credit utilization ratio will show up in your score.

Can you realistically raise your credit score by 100 points in 30 days?

A 100-point boost within a single month is rare but possible under very specific, aggressive conditions. If your score is heavily suppressed because your credit cards are maxed out, paying down those high balances completely can drop your utilization snapshot and trigger a massive, rapid point jump. Similarly, successfully overturning a major reporting mistake through an expedited file dispute can result in an immediate score correction.

How long after a delinquency or collection will my credit score recover?

Rebuilding your standing after a severe mark takes time because late payments and collection records remain visible on your history for up to seven years. However, you do not have to wait seven years to see progress. The mathematical weight of a negative mark diminishes significantly over the first 12 to 24 months, provided you dilute the mistake by layering consistent on-time payments on top of your old files.

How fast will a “hard pull” drop off, and how long does it impact your score?

A hard inquiry stays physically visible on your credit reports for two full years. However, its negative impact on your actual score is short-lived; it generally only influences your score calculation for the first 12 months. The minor point deduction usually fades entirely after a year, as long as you avoid applying for multiple new accounts in a short period.

How long does it take to build a credit history from scratch?

If you are starting out with a “thin file” and have no established borrowing history, it takes a minimum of six months of active reporting for a standard FICO® score to be calculated. Credit bureaus require at least six consecutive months of reported data to accurately weigh your risk level. Opening a secured credit card or a structured credit-builder account is one of the most effective ways to establish this initial data trail safely.

Trust Disclaimer

Credit scoring models and reporting timelines vary by lender and bureau. Loan approval decisions are based on multiple financial factors beyond your credit score, including income, employment history, and debt obligations. Always verify information through official financial institutions or credit reporting agencies.

Conclusion

When you look closely at how long does it take to improve your credit score, it becomes obvious that patience and consistent tracking are your best tools for financial growth. Rebuilding your history is not an overnight process, nor does it require paying an expensive agency to manage your calendar. It is an administrative journey built around regular credit report audits and steady, smart habits. By keeping your credit card balances low, reviewing your credit report data for inaccuracies, and ensuring your bills are paid on time every single month, you can steadily accelerate your recovery timeline. These proactive, defensive steps remove the guesswork from your finances, keeping your files secure and positioning you to reach major life milestones with excellent borrowing power and complete confidence.