Determining the difference between a soft vs hard credit inquiry – impact on credit score outcomes is a vital step for anyone navigating the U.S. financial system. Whether you are shopping for a new car in Texas, applying for a mortgage in Florida, or simply checking your own eligibility for a credit card, the way these credit checks are categorized matters significantly. While some inquiries have zero effect on your creditworthiness, others can cause a temporary dip in your standing. This guide breaks down the realistic timelines and the key factors that distinguish these two types of credit pulls.

Table of Contents

The Speed and Scale of Credit Check Consequences in the USA

Understanding how different credit inquiries affect your financial standing requires a clear understanding of the reporting habits of American lenders. In the modern financial landscape, the credit check is a standard risk-assessment tool used by everyone from local landlords in Chicago to major auto lenders in Los Angeles. However, not all looks at your file are weighted equally by the algorithms that determine your numerical standing.

Soft Inquiries: The Invisible Credit Review

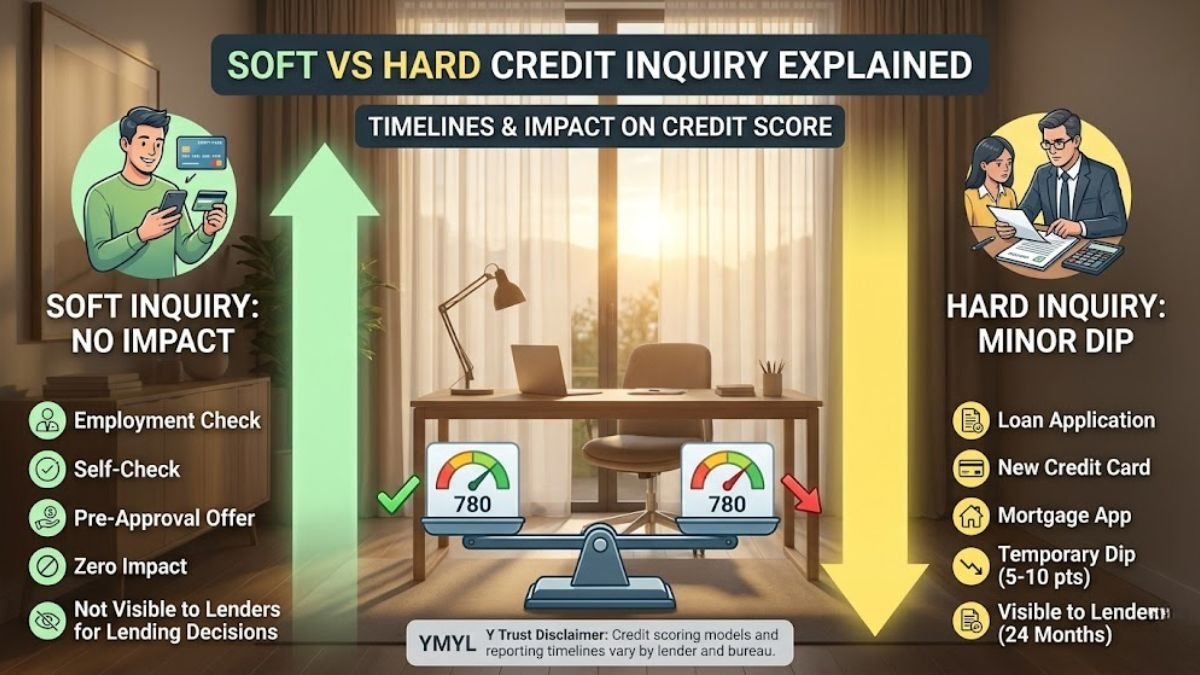

- Employment and Tenant Screenings: These typically occur when a prospective employer in a state like New York reviews your profile or when a property management company performs a basic check.

- Pre-Approval Marketing: Most “pre-qualified” credit card or insurance offers mailed to households across the United States involve a subtle review of your data to determine if you meet initial criteria.

- Speed of Impact: These informational reviews do not affect your credit score.

- Visibility: These are not visible to lenders who review your report for lending decisions, ensuring your privacy during routine checks.

- Monitoring Habits: Accessing your own file frequently through a third-party app or a bank-provided portal is considered a non-impact event.

- Administrative Reviews: When your current credit card issuer checks your file to see if you qualify for a limit increase, it is often logged as a non-harmful event.

Hard Inquiries: The Official Lender Evaluation

- Direct Loan Applications: When you formally apply for a mortgage, auto loan, or a new credit card with a U.S. bank, the creditor performs a hard inquiry to assess risk.

- Speed of Impact: A formal application review generally causes a small, immediate dip in your standing—typically between five to ten points for a single event.

- Duration on File: These records remain on your credit report for exactly 24 months, although their influence on your rating usually diminishes significantly after the first 12 months.

- Rate Shopping Protections: Rate shopping protections allow multiple inquiries for the same type of loan within a short window (typically 14–45 days depending on the scoring model) to be treated as a single inquiry. This helps American consumers find the best deals without being penalized for comparing local lenders.

- Utility and Service Setup: In some cases, utilities or mobile carriers may perform a hard inquiry, though many now use soft checks depending on the provider and the specific U.S. state.

Strategic Analysis of Application Impact Levers

To understand your rankings and the duration required to bolster your credit status, one must look at how various pulls are weighted by the reporting bureaus. Each type of file access has a different speed of impact based on the intent behind the request.

The “New Credit” Category and Lender Risk

In the United States, your financial health is calculated based on five primary pillars. A hard inquiry falls under the “New Credit” category, which accounts for approximately 10% of your total rating. When a lender sees multiple official checks in a short period outside of a rate-shopping window, the algorithm may flag you as a “high-risk” borrower who is seeking excessive debt. This is why a strategic approach to applications is essential for long-term health.

The Monitoring Lever (No Risk)

Informational pulls do not count toward the “New Credit” category at all. This allows you to stay informed about your profile without fear of damaging your standing. In fact, many financial experts recommend checking your report at least once a month to ensure no unauthorized hard inquiries have occurred.

Hard vs. Soft Inquiry Timelines

| Feature | Hard Inquiry | Soft Inquiry |

| Common Trigger | Official Loan Application | Self-Check / Employment |

| Score Impact | Small Dip (5–10 pts) | Zero Impact |

| Visibility to Lenders | Visible for 2 Years | Not visible to lenders who review your report for credit decisions |

| Duration on Report | 24 Months | Varies (Internal use) |

| Impact on Rating | Lasts ~12 Months | None |

| Rate Shopping Deduplication | Supported (14–45 days) | N/A |

Deep Dive: The Anatomy of a Credit Inquiry

When you authorize a lender to look at your data, you are essentially opening a window into your financial history. Here is how the process works across the different bureaus (Equifax, Experian, and TransUnion):

- The Authorization: You sign a digital or physical consent form during a loan application.

- The Request: The lender contacts one or more bureaus to pull your specific file.

- The Record: A hard inquiry is timestamped and recorded under the “Inquiries” section of your report.

- The Calculation: The scoring model (FICO or VantageScore) adjusts your number based on the new inquiry.

- The Aging: Over the next 12 months, the inquiry loses its potency until it eventually has no effect on the score, followed by total removal at the 24-month mark.

Regional Variations and Service Checks

In certain parts of the U.S., like the Northeast or the Pacific Northwest, competition for rental housing is so high that landlords may insist on a hard inquiry rather than a soft one. Before signing any application, always ask which type of check the provider uses. Knowing this answer allows you to preserve your score for when you truly need it, such as when applying for a low-interest mortgage.

Strategic Monitoring: How to Track Your Recovery Timeline

To accurately track your progress and manage the influence on your numerical rating from different reviews, consistent oversight is mandatory:

- Inquiry Audits: Regularly review the “Inquiries” section of your report to ensure all hard inquiries were authorized by you. If you see a check from a company you don’t recognize, it could be a sign of identity theft.

- Identity Protection: Real-time alerts are crucial; an unauthorized application review is often the first sign that someone is attempting to open an account in your name in the U.S.

- Rate Shopping Timing: If you are looking for a major loan, keep your applications within a tight two-week window to take advantage of bureau “deduplication” rules. This is especially helpful for first-time homebuyers who may need to speak with multiple mortgage brokers.

- Official Data Access: Use government-authorized sources like AnnualCreditReport.com to check your reports for free. Since the pandemic, these reports have been available weekly, ensuring you aren’t being penalized for staying informed.

- Freezing Your Credit: If you are not actively looking for a loan, you can “freeze” your files. This prevents any new hard inquiries from being generated, effectively locking your score in place and protecting you from fraud.

Frequently Asked Questions

What is the difference between a soft inquiry and a hard inquiry?

The core difference lies in the intent behind the check and whether it impacts your financial profile. A soft inquiry is a routine background or informational review—such as checking your own rating or a lender evaluating you for a pre-qualified offer—that does not affect your score and is only visible to you. Conversely, a hard inquiry occurs when you formally authorize a lender to review your history for a lending decision, which can temporarily trim a few points from your total standing.

Does checking your own credit score count as a hard inquiry?

No, pulling your own files or checking your consumer metrics through authorized bank applications or designated portals is always classified as a soft credit check. Because self-checks are not tied to a new application for debt, they are mathematically incapable of lowering your score, allowing you to monitor your credit records as frequently as necessary.

How many points does a single hard inquiry take off your credit score?

For the vast majority of consumers with an established financial history, a single hard pull will result in a minimal, temporary reduction of fewer than five points. However, the initial drop can be slightly more pronounced if you possess a thin file with very few reported accounts. Most profiles bounce back completely within a few months, provided you maintain consistent, on-time payment habits.

How long do hard inquiries stay on your credit report?

A hard inquiry will remain visibly timestamped on your credit reports for exactly 24 months from the date of authorization. However, their direct influence on your financial calculation is short-lived; standard FICO® and VantageScore scoring models only factor inquiries from the most recent 12 months into their risk algorithms.

Can multiple inquiries for a mortgage or auto loan ruin your score?

Not if you manage your applications within a short window. Modern scoring models include rate-shopping deduplication rules that allow multiple hard inquiries for the same type of financing—like an auto loan or a mortgage—to be bundled together and treated as a single event. Keeping your shopping comparison timeline within a tight 14 to 45-day bracket ensures you can evaluate multiple lenders without suffering compounding score deductions.

Can a soft credit inquiry happen without your permission?

Yes. Unlike hard inquiries, which legally require your explicit signature or digital authorization, soft credit checks can occur without your direct consent. Credit card companies frequently run unauthorized soft pulls to see if you qualify for promotional pre-approval mailings, and existing creditors use them to periodically review your account standing. Because these reviews point to zero financial risk and do not lower your rating, federal law allows them to occur seamlessly behind the scenes.

Who can see soft inquiries on your credit report?

Only you can see soft credit inquiries when you request your personal consumer disclosure files. Lenders, underwriting algorithms, and third-party financial institutions are completely locked out from seeing these entries when they purchase your file to make a credit decision. Because soft pulls are completely hidden from the public, they have zero influence on your ability to secure a loan or get approved for competitive rates.

Trust Disclaimer

Credit scoring models and the weight of inquiries vary by lender and bureau. Loan approval decisions are based on multiple financial factors beyond inquiries, including income, employment history, and debt-to-income ratios. Always verify information through official financial institutions or credit reporting agencies.

Conclusion

In summary, the distinction between a soft vs hard inquiry – impact on credit score results is determined by whether the review is for informational purposes or an official application for debt. For rapid gains, focus on minimizing unnecessary hard inquiries and keeping your credit applications strategic and timed. Consistent on-time payments, low utilization, and regular monitoring are the foundation of long-term credit improvement. By understanding the technicalities of how the U.S. bureaus report your data, you can navigate your financial journey with confidence and precision.