Starting with no credit history can feel frustrating, especially when lenders want to see a score before approving loans or credit cards. However, learning how to build credit from scratch is completely achievable with the right habits and tools. By establishing a documented track record of borrowing and repayment, you can prove your reliability to financial institutions. Most consumers receive their first credit score after approximately six months of consistent account activity.

Table of Contents

The Best Ways to Establish Your First Credit History

Because you are starting with what lenders call a “thin file”—a profile with very limited data—selecting the right entry-level products is essential for growth. Since you are beginning without a financial history, your payment consistency and how you manage your available credit usage will be the most critical factors for your progress.

Practical Entry Points for New Borrowers

Establishing a financial record requires using specific tools designed for those with no prior borrowing history:

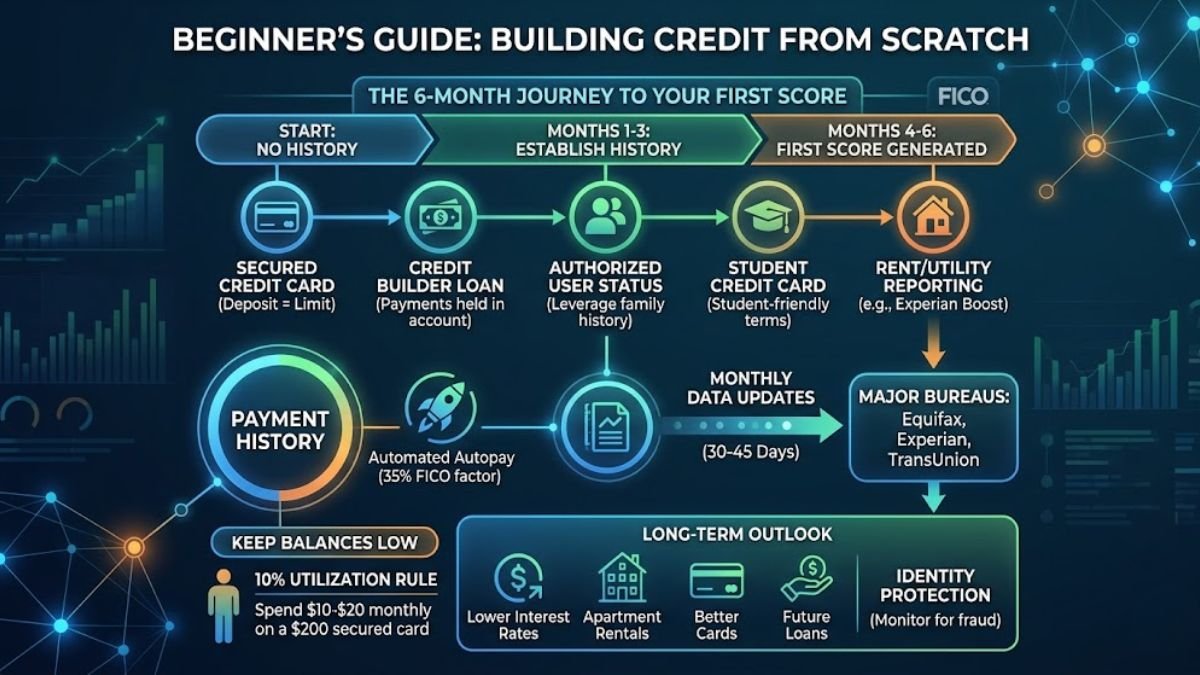

- Secured Credit Cards: These require a refundable security deposit that usually determines your spending limit. They offer a low-risk environment to prove you can manage a card responsibly.

- Credit Builder Loans: Unlike traditional loans, your monthly payments are held in a secure account until the term is complete. The lender reports your consistency to major bureaus like Equifax, Experian, and TransUnion.

- Authorized User Status: In some cases, being added to a family member’s established account with a low balance-to-limit ratio allows you to inherit the benefits of their history.

- Student-Specific Products: Many issuers offer cards for students currently in school. These typically feature lower approval barriers and clear paths to transition into standard accounts.

- Rent and Utility Reporting: Platforms like Experian Boost allow you to add rent and utility payments to your credit record. This can provide a boost for those with limited traditional history.

Understanding the Reporting Lifecycle

To manage expectations, it is vital to understand the timelines involved in credit reporting:

- The Six-Month Timeline: According to FICO, most scoring models require at least 180 days of active data before a formal score can even be generated.

- Monthly Data Updates: Lenders typically transmit your status to bureaus every 30 to 45 days, meaning your progress is updated in predictable monthly cycles.

- The Power of Account Age: While your first account starts the clock, your standing strengthens significantly as your accounts mature over several years.

The Most Important Factors That Affect New Credit

When you have no history, every action has a magnified effect on your credit record. Understanding which factors to prioritize can help you move toward a healthy score more effectively.

Keeping Card Balances Low (Credit Utilization)

- The 10% Utilization Rule: To maximize your standing from the start, experts often suggest keeping your balances below 10% of your total limit.

- Real-World Scenario: For example, if you open a secured card with a $200 deposit, spending around $10–$20 monthly on small purchases and paying the balance in full each month is ideal.

- Manageable Expenses: Many beginners use a small secured card for simple monthly expenses such as streaming subscriptions, fuel, or groceries to keep spending manageable.

- Available Credit Usage: High balances relative to your limits can signal risk to lenders, even if you pay the full amount every month.

The Importance of On-Time Payments

- Automated Systems: Setting up autopay ensures you never miss a due date, protecting your financial profile from late payments.

- FICO Weighting: Payment history is the largest factor affecting most scoring models, accounting for roughly 35% of the total score according to FICO.

Managing New Applications

- Strategic Application Timing: Applying for too many accounts in a short window triggers “hard inquiries,” which can cause your score to dip temporarily.

- Why Keeping Old Accounts Open Matters: The length of your history is a major factor. Keeping your first account active helps lengthen your average account age over time.

Common Mistakes to Avoid

Building a solid financial history requires avoiding pitfalls that can derail your progress early on:

- Missing even one payment: A single 30-day delinquency can stay on your record for up to seven years.

- Maxing out a secured card: High usage on small limits can significantly lower your score.

- Applying for too many cards at once: Each application triggers a hard inquiry, which can look like financial distress to lenders.

- Closing your oldest account too early: This can inadvertently shorten your history and negatively impact your standing.

- Ignoring credit report errors: Incorrect information can unfairly lower your standing.

Comparison: Best Starting Methods

| Method | Ease of Approval | Time to Build History | Main Benefit |

| Secured Card | High | ~6 Months | Revolving Credit History |

| Credit Builder Loan | High | ~6 Months | Payment History |

| Authorized User | Variable | 1–2 Billing Cycles | Faster Account Aging |

| Student Card | Moderate | ~6 Months | Beginner-Friendly Credit |

How to Track and Protect Your Growing Profile

Keeping a close eye on your data ensures your efforts are being recorded accurately and protects you from fraud.

- Audit Your Reports: Use government-authorized sites, such as AnnualCreditReport.com, to ensure your new accounts appear correctly on all three major bureaus.

- Monitor Card Balances: Use your bank’s built-in tools to watch your credit usage and see how it correlates with your score in real-time.

- Identity Protection: Establishing security habits, such as monitoring for unauthorized accounts, is vital for protecting an emerging credit record from fraud.

Frequently Asked Questions

- Can you build credit with a debit card? Generally, no, as debit card activity is not typically reported to the major credit bureaus.

- Does checking your own credit lower your score? No, checking your own score is a “soft inquiry” and does not impact your standing.

- What happens if you miss your first payment? Missing a payment can significantly damage your financial profile and stay on your record for up to seven years.

- Is it bad to open multiple cards at once? Yes, for a beginner, multiple rapid applications can signal financial risk and lower your score.

Trust Disclaimer: Credit scoring models and reporting timelines vary by lender and bureau. Approval for any credit product is based on various factors, including income and employment, not just your initial score. Always verify details with official financial institutions or the Consumer Financial Protection Bureau (CFPB).

Conclusion

Building credit takes time, but small, consistent habits can make a major difference over the long term. By starting with the right tools like secured cards or credit builder loans and keeping your balances low, you establish a solid foundation for future growth. Following these recognized guidelines from institutions like FICO can eventually help you qualify for lower interest rates, better credit cards, apartment rentals, and future loans.