Determining how to improve your credit score quickly is a critical objective for many consumers in the United States looking to unlock better financial opportunities. In the current financial climate, your credit rating is the engine behind your purchasing power. Whether you are preparing to enter the housing market or seeking a more competitive interest rate on a personal loan, a 100-point shift in your standing can be the difference between a “subprime” designation and “preferred” borrower status.

While credit building is often described as a long-term marathon, certain “mechanical” updates to your profile can yield rapid results. If your score is currently suppressed by high utilization or correctable reporting errors, a 100-point increase is a logical outcome of targeted optimization. By focusing on the factors that carry the most mathematical weight, you can often shift your standing in weeks rather than years.

Table of Contents

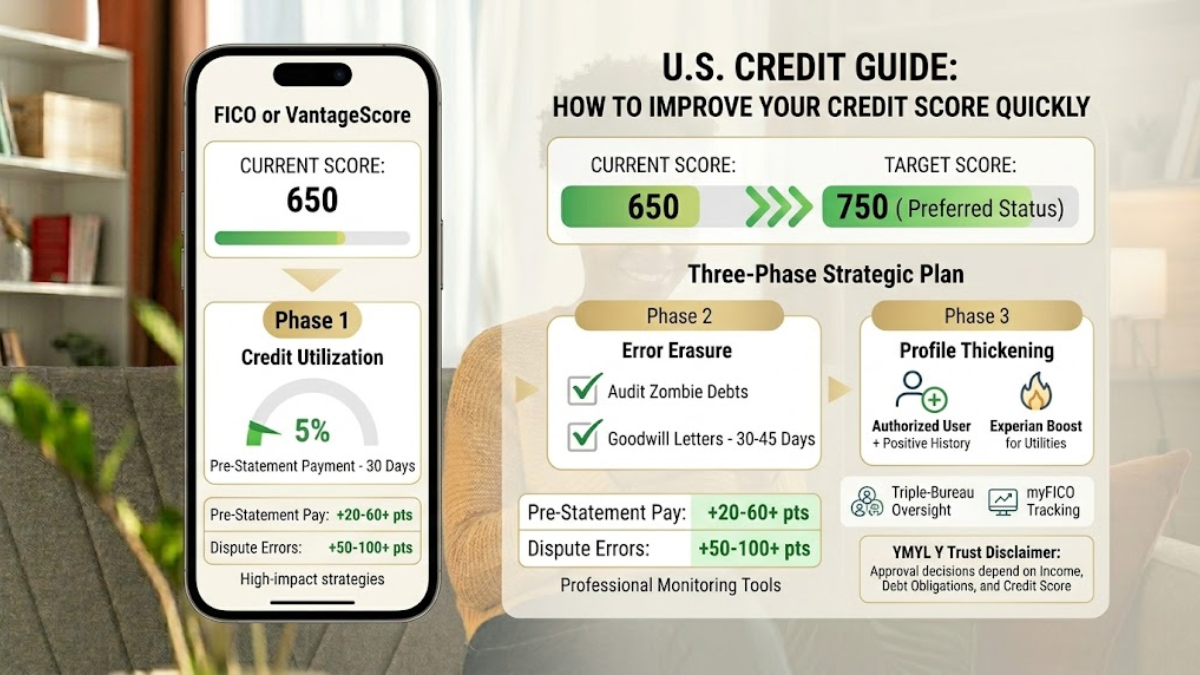

Strategies for Elevating Your Standing via Utilization Adjustments

Your Credit Utilization Ratio—the amount of revolving credit you use compared to your limits—accounts for approximately 30% of your total score. This is one of the fastest “levers” available for those looking at how to improve your credit score quickly.

The Pre-Statement Payment Maneuver

- Most consumers pay their bills by the due date.

- However, lenders report your balance to the bureaus on the statement closing date.

- If you pay your balance in full three days before the statement closes, the bureau sees a 1%–3% utilization rate rather than a high balance.

- This move may help some consumers see noticeable improvement in one billing cycle.

The “Micropayment” Approach

- Instead of one large monthly payment, make small payments throughout the month.

- This keeps your average daily balance low and prevents utilization “spikes” that modern scoring models often flag as high-risk behavior.

Requesting a Limit Increase

- Contact your card issuer and request a higher limit without a “hard pull”.

- If your limit increases while your balance remains steady, your utilization percentage instantly drops, which often results in an immediate lift.

Note on Tracking: To track how quickly these utilization changes affect your standing, many people use credit monitoring tools that provide regular updates and alerts when balances change. This allows you to verify that lenders are reporting your lower balances accurately each month.

Rapid Error Erasure for Improving Your Score

According to the Consumer Financial Protection Bureau (CFPB), a significant percentage of credit reports contain errors that negatively impact scores. Erasing a single misplaced late payment can often provide a substantial boost.

Auditing for “Zombie” Debts

- Review your reports from Equifax, Experian, and TransUnion for debts that are older than seven years.

- These should typically drop off automatically; if they remain, a formal dispute under the Fair Credit Reporting Act (FCRA) can lead to their removal.

The “Goodwill” Letter Technique

- If you have a single late payment on an otherwise perfect account, contact the lender.

- Many creditors may remove a one-time late payment as a courtesy for loyal customers.

- This is a “soft” negotiation that can offer high rewards without legal filing.

Addressing Personal Data Mismatches

- Inaccuracies in your personal data, such as misspelled names or old addresses, can lead to “mixed files” where another person’s negative history is attached to your name.

- Cleaning up your personal information section is a foundational step for recovery.

Comparison: High-Impact Strategies for Quick Results

| Strategy | Primary Factor | Estimated Speed | Potential Impact |

| Pre-Statement Pay | Utilization | 30 Days | High (20-60+ points) |

| Dispute Errors | Payment History | 30-45 Days | Very High (50-100+ points) |

| Authorized User | Credit Age | 30 Days | High (30-80+ points) |

| Experian Boost™ | Credit Age / Mix | Instant | Moderate (5-15 points) |

Strategic Tactics to Thicken Your Profile Fast

If your score is low because of a “thin file” (not enough credit history), you may need to add positive data points quickly. This is a core component of how to improve your credit score quickly.

The Authorized User Route

- If a family member with a long-standing, high-limit credit card adds you as an “authorized user,” that account’s positive history can be mirrored onto your report.

- You do not necessarily need to use the card to benefit from the age and low utilization it provides.

Incorporating Utility Payments

- Many modern scoring models now incorporate alternative data.

- Using services like Experian Boost™ allows you to add your on-time rent, utility, and even streaming service payments to your report, which can provide an immediate lift.

Credit-Builder Loans

- For those with no active credit history, a credit-builder loan—where funds are held in a secure account while you make payments—can establish a positive payment history without the risk of high-interest revolving debt.

Understanding the “Trended Data” Shift in the US

The lending industry has moved toward more predictive analysis. Modern scoring models increasingly look at your 24-month trajectory rather than just a current snapshot.

- Historical View: Paying off a debt today used to result in an immediate jump.

- Trended View: Lenders now reward a consistent downward trend in debt. To see a 100-point move that lasts, it is beneficial to show that your balances are consistently decreasing month-over-month.

Frequently Asked Questions

What is the absolute fastest way to improve your credit score quickly?

The most immediate method to jumpstart your credit score quickly is to dramatically lower your credit utilization ratio. Paying down high credit card balances right before your statement closing date—rather than your actual due date—forces the credit bureaus to record a low debt-to-limit ratio for that billing cycle. If you lack the cash to pay down balances immediately, being added as an authorized user to a family member’s long-standing, low-balance credit card can mirror their excellent history onto your profile in about 30 days.

How long does it take to see a 100-point increase in your credit score?

A rapid 100-point lift is highly achievable within 30 to 45 days if your current score is being artificially suppressed by fixable, high-impact issues. These include extreme credit card utilization spikes or severe reporting errors on your history. Correcting a major mistake (like a fraudulent collection account or an incorrect late payment) through an official dispute can trigger an immediate, massive point correction the moment the bureau clears the error from your file.

Does paying off an old collection account instantly raise your score?

The impact of paying off a collection account depends entirely on the specific scoring model a lender pulls. Newer algorithms automatically ignore collection balances once they are paid in full. However, older scoring models—which are still widely utilized for mortgage lending decisions—will continue to penalize your score for the collection mark even after it is paid. To fix this under older systems, you must negotiate a “pay-for-delete” agreement with the collection agency before sending payment.

How many points does a single late payment drop your credit score?

For someone with an excellent credit profile, a single 30-day late payment can cause an immediate and devastating drop of 60 to 100 points. Because payment history is the single largest component of your score calculation, even a one-time oversight signals a sudden risk shift to automated scoring models. If this happens on an otherwise flawless account, you should mail a “goodwill letter” to the creditor asking them to remove the late mark as a courtesy.

Can raising your credit card limit help improve your credit score quickly?

Yes. If you contact your credit card issuer and secure a credit limit increase, your overall credit utilization ratio drops instantly—provided you keep your spending balances exactly the same. When requesting an increase, explicitly ask the representative if the review requires a “soft pull” or a “hard pull.” Opting for issuers that grant limit increases via soft pulls ensures you gain the mathematical utilization boost without risking a temporary hard inquiry deduction.

Professional Tools for Monitoring Your Progress

Consistent oversight is necessary to ensure the bureaus are reflecting your updates correctly during this process.

- For Official Data: AnnualCreditReport.com remains the government-authorized source for your full reports.

- For Triple-Bureau Oversight: Professional services provide real-time alerts across all three bureaus, helping to ensure that no new negative information interferes with your improvement efforts.

- For FICO Tracking: Specific platforms allow you to see exactly how your changes are impacting the scores lenders use for mortgage and auto decisions.

The Discipline Required for a Rapid 100-Point Move

Learning how to improve your credit score quickly is a methodical process of removing negatives and optimizing positives. By leveraging strategies like the utilization adjustment strategy and clearing reporting errors through your rights under the FCRA, you are not just chasing a number—you are reclaiming your financial reputation.

Consistent monitoring helps you stay prepared for important financial decisions and reduces the risk of unexpected issues. If you’re actively working toward a 100-point increase, using a professional monitoring tool can help you see which changes are working in real time and protect your progress from fraud. In today’s economy, maintaining a strong credit profile matters more than ever. A strong credit score is one of the most valuable financial tools you can have. Start by auditing your report and paying down a single balance before the statement closes; often, the momentum of that first 20-point jump provides the foundation for the journey to 100.

Conclusion

Mastering how to improve your credit score quickly requires a blend of technical optimization and behavioral consistency. By prioritizing the “mechanical” levers like utilization ratios and error removal, you can encourage scoring models to reflect your improved profile more quickly. This rapid shift from a subprime rating to preferred borrower status is a foundational step toward achieving significant financial milestones, such as securing a mortgage with a competitive interest rate. Ultimately, maintaining this new threshold depends on the long-term discipline of on-time payments and proactive credit monitoring, ensuring your creditworthiness remains a powerful asset rather than a liability.