Understanding exactly how credit utilization affects your credit score is a critical component of mastering your personal finances. Credit utilization represents the percentage of your available revolving credit that you are currently using across your accounts. Because this crucial metric accounts for 30% of your total credit score, it stands as the second most important element in your financial file, trailing only your history of consistent, on-time payments. The speed at which your credit score responds to changes in your debt levels depends entirely on monthly lender data transmission cycles. By breaking down how your debt-to-limit ratio influences your credit profile, you can utilize high-impact strategies—like strategic payment timing and credit limit updates—to optimize your borrowing power. This comprehensive guide outlines the realistic timelines for financial recovery and the key factors that dictate how revolving debt shapes your score.

Table of Contents

The Impact of Revolving Debt Balances on Your Credit Score

Managing your balances effectively requires understanding how scoring models interpret your borrowing habits. Over time, your utilization habits play a major role in shaping your credit score.

Ideal Credit Utilization Ratio

- Practical Example: If your total credit limit is $10,000 and your balances equal $2,000, your debt-to-limit ratio is 20%.

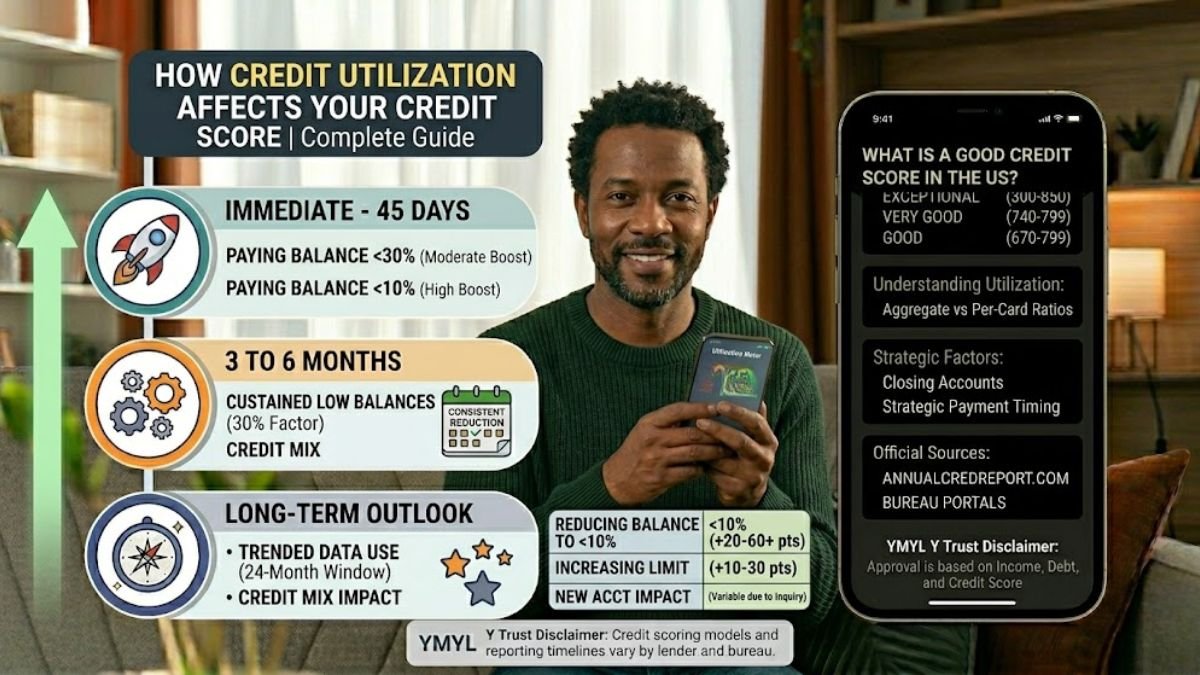

- The 30% Benchmark: Financial institutions generally recommend keeping your total revolving debt below 30% of your available limits to avoid a negative impact on your credit score.

- The “Exceptional” Threshold: To enter elite credit score tiers (800+), most borrowers maintain an aggregate utilization percentage of less than 10%.

- Aggregate vs. Per-Card Ratios: Scoring models analyze both your total combined debt across all accounts and the specific revolving usage of each individual card.

- The “Zero Balance” Trap: Having a 0% utilization rate across all accounts can sometimes result in a lower credit score than a very small, active balance because it shows a lack of activity.

Reporting Timing and Your Credit Profile

- Statement Closing Date Importance: Your utilization rate is usually calculated based on the balance reported on your statement closing date.

- Reporting Cycle Timing: Most lenders transmit debt data to major bureaus once per month, usually within 30 to 45 days of your last statement.

- Immediate Recovery Potential: Unlike payment history, your revolving usage updates almost immediately once a lower balance is reported, potentially boosting your credit score quickly.

- Statement Balance vs. Current Balance: Because of reporting delays, the credit score you see today might be based on a debt-to-limit ratio from several weeks ago.

Credit Limit Effects on Your Credit Score

- Credit Limit Increases: Requesting an increase in your credit limit is one of the fastest ways to lower your utilization percentage without paying down debt.

- New Account Influence: Opening a new revolving account increases total available credit, which can lower your overall utilization rate once the account appears on your credit profile.

- Closing Account Consequences: Closing a card reduces your total available limit, which can cause a spike in your revolving usage and a dip in your credit score.

- Impact of Denied Limit Increases: Requesting more credit can trigger a hard inquiry, which may cause a minor temporary dip in your credit score.

Strategic Payment Timing for a Better Credit Score

- Strategic Balance Paying: Paying your bill a few days before the statement closing date ensures a lower balance is reported, helping lower your reported utilization rate.

- Trended Data Evolution: Modern scoring models now look at whether your debt-to-limit ratio is increasing or decreasing over a 24-month window.

- Authorized User Benefits: Being added to a card with a high limit and low balance can instantly lower your aggregate utilization percentage, improving your credit score.

Strategic Analysis of Outstanding Debt Levers

To understand the duration required to bolster your credit score, one must look at the mathematical weighting of the reporting bureaus.

- The Usage Lever (Fastest Speed): This accounts for 30% of your total credit score. Paying down a card today can result in a significant credit score jump as soon as the next month.

- The Account Age Lever (Slowest Speed): Closing a card to “clean up” your wallet can hurt your utilization rate and shorten your average age of accounts (15% of your credit score).

- The New Credit Lever (Immediate Impact): Applying for credit to help your revolving usage can backfire if the hard inquiry causes a dip in your credit score larger than the gain from the new limit.

Comparison: Timelines for Credit Utilization Adjustments

| Action Taken | Estimated Time for Impact | Potential Credit Score Impact |

| Paying Balance to Under 10% | 30–45 Days | High (20-60+ points) |

| Increasing Credit Limit | 30–60 Days | Moderate to High |

| Opening New Revolving Account | 30–60 Days | Variable (due to inquiry) |

| Closing an Unused Card | 30–45 Days | Negative (due to lower limits) |

| Authorized User Addition | 30–60 Days | High (30-80+ points) |

The Lifespan of High Usage Marks on Your Credit Profile

While severe marks like late payments stay for years, the impact of debt levels on your credit score can change quickly.

- Memoryless Models: Traditional FICO models do not penalize your credit score for a high utilization rate in the past once that balance is paid off.

- Trended Reporting: Newer models track whether your utilization percentage is rising or falling over two years, rewarding consistent debt reduction.

- Statement Cycles: Your revolving usage is essentially “reset” every 30 days in the eyes of the bureaus based on new data.

Strategic Monitoring: How to Track Your Credit Score Timeline

To manage the impact of borrowing levels on your credit profile, consistent oversight is mandatory:

- Statement Closing Date Identification: Use your bank’s app to identify your statement close date so you can pay early and optimize your reported utilization rate.

- Weekly Audits: Weekly checks allow you to see exactly when a lower debt-to-limit ratio is officially recorded during a recovery phase.

- Score Tracking Tools: Utilize tools to see how your revolving usage correlates with your credit score in real-time.

- Identity Protection: A sudden spike in your utilization rate is often an early sign of a compromised account.

Frequently Asked Questions

Why does credit utilization affect your credit score so much?

Credit utilization is heavily weighted because it serves as a direct barometer of your current financial stability. Credit scoring models utilize this percentage to determine how reliant you are on revolving debt; a high ratio signals to potential lenders that you may be facing financial pressure or overspending. Because it accounts for 30% of your total credit score, keeping this ratio low is one of the most effective ways to prove you can manage open lines of credit responsibly.

Is a 0% credit utilization ratio good for your credit score?

Counterintuitively, a 0% utilization rate is actually less ideal than a small, active percentage like 1% to 10%. Credit scoring models require some baseline activity to evaluate your credit habits. When all your revolving accounts show a flat zero balance on their statement closing dates, the system interprets it as a lack of usage rather than responsible management, which can cause your score to dip slightly.

Does credit utilization look at individual cards or total combined credit?

Scoring models look at both your aggregate (total combined) credit utilization and your per-card utilization. Having a low overall ratio will not completely protect your credit score if a single card is maxed out. Lenders look at individual account limits as well, so spreading your expenses or keeping balances uniformly low across all individual accounts is crucial for maximizing your rating.

How quickly can lowering my credit utilization improve my credit score?

Unlike your payment history, which takes months to dilute older mistakes, your credit utilization lever is essentially “memoryless” and resets every 30 days. As soon as your lender transmits your lower balance to Equifax, Experian, and TransUnion, the updated ratio is recorded. This means you can typically see an upward shift in your credit profile within a 30 to 45-day window.

Does a high credit utilization ratio matter if I pay my bill in full every month?

Yes, it can still lower your score. Lenders report your data to the credit bureaus once a month, typically on your statement closing date—not your payment due date. If you make a large purchase and let that high balance sit until your statement prints, that elevated utilization percentage is what gets officially reported, even if you pay the entire balance off to zero a few days later. To avoid this, try submitting a payment a few days before your statement closing date.

Trust Disclaimer

Credit scoring models and reporting timelines vary by lender and bureau. Loan approval decisions are based on multiple financial factors beyond your credit utilization ratio. Always verify information through official financial institutions.

Conclusion

When you look closely at how credit utilization affects your credit score, it becomes obvious that your debt-to-limit ratio is one of the most manageable levers in your entire financial file. Because traditional scoring models look at your balances as a monthly snapshot, improving your history does not require waiting years for old marks to fade or paying a commercial repair business to manage your files. It is an administrative task that responds rapidly to simple consistency and strategic payment timing. By paying down your revolving balances, keeping your accounts open to preserve your total credit limit, and timing your payments to post before your statement closing dates, you can steadily accelerate your score’s recovery timeline. These practical, defensive steps remove the stress from managing your history, keep your records secure, and position you to approach major life milestones with excellent borrowing power and complete confidence.