In the complex financial landscape of the United States, your three-digit credit rating is arguably your most valuable asset. It acts as a financial passport, determining whether you can secure a mortgage, lease a vehicle, or even land certain professional roles. But a question often arises: What is a good credit score in the US? The answer is not a single static number, but rather a range that varies depending on the scoring model used and the specific requirements of lenders. This comprehensive guide explores the tiers of credit excellence, the mechanics behind these numbers, and actionable strategies to ascend the ranks of creditworthiness.

Table of Contents

Understanding the Thresholds of Credit Excellence

Most lenders in the U.S. rely on two primary scoring systems: FICO and VantageScore. While both use a scale of 300 to 850, the definition of a “good” status can differ slightly between them.

The FICO Score Ranges

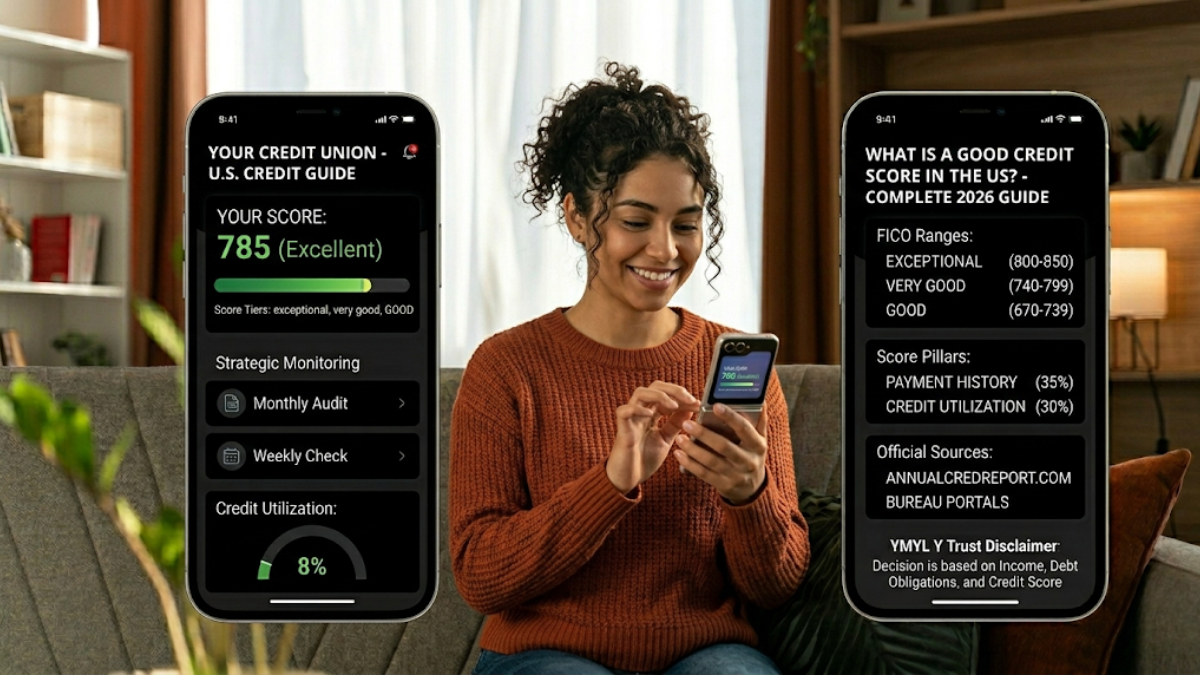

FICO remains the industry standard, utilized by approximately 90% of top lenders.

- Exceptional (800–850): Borrowers in this range are considered “elite” and qualify for the lowest possible interest rates.

- Very Good (740–799): This tier suggests a highly reliable borrower profile with very low risk to lenders.

- Good (670–739): This is the national average range. Most lenders consider this a safe bet for standard loan products.

- Fair (580–669): Borrowers here may face higher interest rates and more restrictive terms.

- Poor (300–579): Often indicative of significant past delinquencies; securing new credit in this range is difficult.

The VantageScore Ranges

VantageScore is a collaborative model created by the three major bureaus—Equifax, Experian, and TransUnion.

- Excellent (781–850): Comparable to FICO’s top tier for securing premium financial rewards.

- Good (661–780): A broader range that captures the majority of reliable consumers.

- Fair (601–660): Indicates moderate risk; lenders may require larger down payments.

- Poor (300–600): Reflects a high-risk history that requires active credit monitoring and repair.

How Your Standing Impacts Your Daily Life

A “good” rating is more than just a badge of honor; it has tangible economic consequences for your consumer credit metrics.

1. Lower Interest Rates (APR)

The difference between a 650 and a 750 score on a 30-year mortgage can translate into tens of thousands of dollars saved in interest over the life of the loan. Lenders reserve their “prime” rates for those in the Very Good and Exceptional categories.

2. Insurance Premiums

In many states, auto and home insurance companies use credit-based insurance scores to determine your premiums. A higher rating often correlates with lower insurance costs.

3. Rental Opportunities

Landlords routinely perform a soft credit check to assess a potential tenant’s reliability. A poor score can lead to a rejected application or a requirement for a much higher security deposit.

The Pillars of a Strong Credit Profile

To understand how to reach a “good” status, you must analyze the scoring factors that build your rating.

- Payment History (35%): The most critical factor; even one 30-day late payment can cause a significant dip.

- Credit Utilization (30%): This is the ratio of your balances to your total limits. Aiming for a debt-to-limit ratio below 10% is ideal for high-tier scores.

- Length of Credit History (15%): The age of your oldest and newest accounts matters. Maintaining long-term accounts is beneficial for your credit file.

- Credit Mix (10%): Lenders like to see a variety of accounts, such as a mortgage (installment) and a credit card (revolving).

- New Credit Inquiries (10%): Multiple hard pulls in a short period can signal financial distress and temporarily lower your score.

Strategic Monitoring: How Often Should You Check?

To maintain a good standing, you must ask: How often should you check your credit score?.

- Monthly Routine: For general health, a monthly audit is recommended to track billing cycle updates and ensure accuracy.

- Pre-Purchase Strategy: If buying a home, check weekly starting six months before your application to optimize your credit utilization.

- Fraud Prevention: Checking your report is the fastest way to detect identity theft or unauthorized accounts.

Remember, viewing your own profile is a soft inquiry, which means you can check it daily without any negative impact on your numbers.

Comparison: Benefits of Different Score Tiers

| Score Tier | Loan Approval Odds | Interest Rate Tier | Required Down Payments |

| 800–850 | Extremely High | Lowest (Prime) | Minimal requirements |

| 740–799 | High | Low (Near-Prime) | Standard requirements |

| 670–739 | Moderate | Average | Standard to higher |

| 580–669 | Low | High (Subprime) | Often requires 20%+ |

| Below 580 | Very Low | Highest | Secured loans only |

Official Sources for Your Information

You can access your detailed history and current standing through these authorized channels:

- AnnualCreditReport.com: The official site for free reports from the national bureaus.

- Bank Apps: Most major U.S. banks now offer free FICO score tracking.

- Bureau Portals: Direct access via Experian, Equifax, or TransUnion for real-time alerts on your credit file.

Frequently Asked Questions (FAQ)

What is considered a good credit score range in the US?

Under the industry-standard FICO® model, a credit score between 670 and 739 is officially categorized as “Good”. If you are looking at your VantageScore® tracking metrics, a “Good” rating spans from 661 to 780. Scores exceeding these thresholds move you into the “Very Good” and “Exceptional” brackets, unlocking optimal financial terms.

What minimum credit score do you need to buy a house or a car?

There is no single magic number required for auto financing or home approval, as requirements vary by lender and program. For conventional mortgages, standard lenders typically look for a minimum score of 620, though government-backed options like FHA loans can accept scores as low as 500 to 580 with a larger down payment. For auto loans, a score of 661 or higher generally positions you to receive favorable terms and affordable interest rates.

Can you check your credit score for free without hurting it?

Yes. Whenever you review your own credit profile through online banking dashboards, personal finance apps, or authorized data portals, the action is classified as a soft inquiry. Because you are not actively applying for a new line of debt, these routine checks have zero impact on your credit rating and will never drop your score by a single point.

How long do negative marks stay on your credit history?

Most standard negative items, including late payments, missed billing cycles, and accounts sent to collections, legally remain on your credit files for seven years from the date of the original delinquency. Bankruptcies can stay on your profile slightly longer, lingering for up to ten years depending on the specific filing type.

Why does a credit score suddenly drop after paying off a loan?

It is common to see a temporary decline in your points immediately after closing an active debt account. This happens because closing an installment loan can reduce your overall credit mix (the variety of accounts you manage) or shorten the average age of your active accounts. While frustrating, this minor dip is standard and usually corrects itself over the following billing cycles.

Trust Disclaimer

Credit scoring models and reporting timelines vary by lender. Loan approval decisions are based on multiple financial factors beyond your credit score, including income, employment history, and debt obligations. Always verify your specific status through official financial institutions or credit reporting agencies.

Conclusion

A good credit score is the cornerstone of financial freedom in the U.S.. By understanding credit score ranges, monitoring your profile consistently, and maintaining strong payment habits, you can ensure your financial resume is always ready for the next big opportunity. Whether you are a “Passive Saver” checking quarterly or a “Prospective Homebuyer” monitoring weekly, staying proactive is the only guaranteed way to maintain an exceptional rating.